Introduction

In the digital age, technology is advancing speedier than ever some time recently, and one of the most groundbreaking developments is blockchain. But what precisely is blockchain, and why is it such a huge deal?

At its core, blockchain is a technology that permits for secure, straightforward, and decentralized information sharing. It’s the engine behind cryptocurrencies like Bitcoin and Ethereum, but its potential goes distant past fair digital currencies. Blockchain is balanced to revolutionize businesses like finance, healthcare, supply chain, and indeed voting systems by making forms more proficient and transparent.

Imagine a world where you don’t have to depend on banks, middlemen, or government authorities to confirm and approve exchanges. A world where believe is built specifically into the system. That’s what blockchain promises to deliver.

In this direct, we’ll break down blockchain in basic terms so you can understand how it works, why it’s imperative, and how it’s changing the way we live and do commerce. Whether you’re a total fledgling or fair inquisitive about blockchain, you’ll find everything you require to know right here.

What is Blockchain?

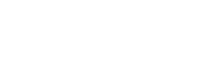

At its core, blockchain is a type of digital ledger or record-keeping system. Think of it like a note pad, but instep of being put away in one put, duplicates of it are put away across thousands of computers around the world.

The word “blockchain” comes from the way this technology works — it’s a chain of pieces, and each block contains a list of exchanges. When new exchanges happen, they’re assembled together in a block. Once a block is full, it’s included to the chain in a way that can’t be changed. That’s what makes it so secure.

Unlike traditional databases that are controlled by a central authority (like a bank or a company), blockchain is decentralized. That means no single individual or bunch has control over the entire blockchain. Instep, everybody in the organize has access to the same data, and changes can as it were be made if there’s agreement across the system — this is called consensus.

To simplify even more:

- Imagine a Google Sheet that’s duplicated thousands of times across a network of computers.

- Every time a change is made, all the copies update automatically.

- There’s no central version — it’s shared and transparent.

Because of this, blockchain is often praised for being:

- Transparent: Everyone on the network can see the data.

- Secure: Once information is added, it can’t be altered without changing every block that comes after it (which is extremely difficult).

- Trustworthy: There’s no need for a middleman — the technology itself ensures accuracy and trust.

So, in simple terms, blockchain is a secure and transparent way to record, share, and store data — and it’s changing how we think about trust in the digital world.

How Does Blockchain Work?

Presently that you know what blockchain is, let’s break down how it actually works — step by step.

Imagine you need to send money to a friend utilizing a blockchain-based system like Bitcoin. Here’s what happens behind the scenes:

1. A Transaction is Requested

You start a exchange — for case, you need to send 0.5 Bitcoin to your friend. This exchange includes details like:

- Who is sending the money

- Who is receiving it

- How much is being sent

2. The Transaction is Shared with the Network

The transaction is broadcast to a network of computers, known as hubs. These computers are spread out over the world and are all portion of the blockchain system.

3. Validation by Nodes (Consensus)

The hubs check the exchange to make beyond any doubt it’s true blue — for case, they affirm that you really have the Bitcoin you’re attempting to send. This is done utilizing complex calculations and is known as consensus.

There are different methods to achieve consensus:

- Proof of Work (PoW): Computers race to unravel a mathematical puzzle. The to begin with one to unravel it gets to include the block to the chain.

- Proof of Stake (PoS): Instep of dashing, validators are chosen based on how much cryptocurrency they hold and are willing to “stake” as confirmation of honesty.

4. The Transaction is Added to a Block

Once the exchange is confirmed, it gets gathered with other exchanges to shape a modern block. Think of this block as a new page in the digital ledger.

5. The Block is Added to the Chain

The new block is linked to the past block utilizing a extraordinary code called a hash. This makes a secure connection between blocks, shaping a chain of blocks — thus the name blockchain.

6. The Upgrade is Shared Over the Network

Once the block is included, it’s obvious to everybody on the network. The exchange is presently complete, and the record is lasting — it can’t be changed or erased.

Key Components of Blockchain

To truly understand how blockchain works, it’s important to know the key parts that make up the system. Here are the main components of a blockchain, explained in simple terms:

1. Blocks

A block is like a digital container that holds a list of transactions. Each block has three main elements:

- Data: This is the actual information being recorded (like who sent what to whom).

- Hash: A unique digital fingerprint or ID for the block.

- Hash of the Previous Block: This connects the current block to the one before it, forming a chain.

Together, this setup ensures that no block can be altered without affecting all the others — making the chain secure.

2. Chain

When blocks are linked together, they form a chain — thus the name blockchain. 2 .Each new block is associated to the one some time recently it utilizing cryptographic hashes. This structure guarantees the keenness and order of the data.

3. Decentralization

Unlike conventional systems where a single specialist (like a bank) controls everything, blockchain is decentralized. That means the information isn’t stored in one put — instep, it’s distributed over a network of computers (called nodes).

This makes blockchain:

Hard to hack (you’d have to hack thousands of computers at once)

Transparent (everybody can see the same data)

Trustworthy (there’s no single point of failure)

4. Nodes

Nodes are person computers that take an interest in the blockchain organize. 3 .Each hub has a full or fractional duplicate of the entire blockchain and makes a difference confirm new exchanges. Hubs work together to maintain the network and ensure everything runs smoothly.

5. Consensus Mechanisms

Since there’s no central specialist, blockchain employments special rules called agreement mechanisms to concur on what’s genuine. These instruments make sure that all the hubs on the network agree some time recently including unused data.

Two common types are:

- Proof of Work (PoW): Used by Bitcoin. Computers solve complex puzzles to validate transactions.

- Proof of Stake (PoS): Validators are chosen based on the sum of cryptocurrency they hold and are willing to “lock up” or stake.

6. Cryptography

Blockchain uses cryptographic techniques to secure data and ensure privacy. Each user has a pair of keys:

- A public key (like your account number)

- A private key (like your password)

These keys help users send and receive transactions securely.

Real-World Applications of Blockchain

Blockchain isn’t just about Bitcoin. Whereas it started as the technology behind cryptocurrencies, it has since advanced into a capable tool with a wide range of applications across many businesses. Let’s see at how blockchain is being utilized in the real world today.

1. Cryptocurrencies (e.g., Bitcoin, Ethereum)

The most well-known utilize of blockchain is in cryptocurrencies. Bitcoin was the first digital currency to utilize blockchain, permitting people to send and receive money without the require for a bank. Other cryptocurrencies like Ethereum have taken it assist by supporting smart contracts — programs that run naturally when certain conditions are met.

2. Supply Chain Management

Blockchain is revolutionizing the way we track goods from generation to conveyance. In a supply chain, each step — from manufacturing to shipping — can be recorded on the blockchain, making it simple to confirm where a item has been and whether it’s authentic.

Example:

- Walmart employments blockchain to track nourishment items from cultivate to rack, making a difference to recognize defilement rapidly and progress nourishment safety.

3. Healthcare

In the healthcare industry, blockchain can securely store and share persistent records. Since medical data is delicate, utilizing blockchain guarantees that information is exact, tamper-proof, and only open to authorized people.

Example:

- Hospitals can utilize blockchain to allow doctors and patients secure access to restorative history, decreasing mistakes and progressing treatment.

4. Banking and Finance

Blockchain empowers quicker and more secure monetary exchanges without the require for middlemen like banks or clearinghouses. It decreases costs, speeds up exchanges, and gives transparency.

Examples:

- Cross-border payments utilizing blockchain can be completed in minutes instead of days.

- Decentralized finance (DeFi) platforms permit people to borrow, loan, and exchange crypto resources without a traditional bank.

5. Voting Systems

Blockchain can be utilized to construct secure and transparent voting systems. Since blockchain records are about impossible to alter with, votes can be followed and verified without risking extortion or manipulation.

Example:

- Some nations and cities have tested blockchain-based voting apps to permit farther, secure voting in elections.

6. Digital Identity

Blockchain can help people control their digital personalities. Instep of depending on different passwords and logins, individuals might utilize blockchain to confirm their personality securely over different services.

Example:

- A blockchain-based ID might permit you to sign up for a service, apply for a credit, or travel without carrying different documents.

7. Real Estate

In real estate, blockchain can be utilized to record property exchanges, making the buying and offering handle faster, cheaper, and more straightforward. It can decrease paperwork, cut out middlemen, and lower the chance of fraud.

Why Blockchain Matters

In today’s digital world, trust, transparency, and security are more important than ever. This is exactly where blockchain technology stands out — it offers a new way to store and share information that doesn’t rely on middlemen or centralized authorities.

Let’s explore why blockchain truly matters and why it’s gaining so much attention across industries.

1. Trust Without Intermediaries

Traditionally, we’ve relied on third parties like banks, governments, or companies to verify and manage our transactions. Blockchain changes that. It allows people to trust the system itself, not a person or institution. Because of its transparent and secure design, blockchain creates trust between users — even if they don’t know each other.

2. Transparency

Every transaction on a blockchain is visible to all participants and permanently recorded. This means:

- You can track what happened, when, and by whom.

- There’s no hidden data or manipulation behind the scenes.

This level of openness builds accountability in systems like finance, supply chains, and governance.

3. Security

Blockchain uses cryptographic techniques to protect data. Once information is added to the blockchain, it cannot be changed without altering every single block after it — which is nearly impossible. This makes blockchain extremely secure and tamper-resistant.

It’s especially valuable for industries where data accuracy and protection are critical, such as healthcare, finance, and legal services.

4. Reduced Costs and Increased Efficiency

By removing middlemen and automating processes through smart contracts, blockchain reduces the time, cost, and complexity of many operations. For example:

- Sending money internationally takes minutes instead of days.

- Verifying documents or identities can happen instantly and securely.

5. Empowering Individuals

Blockchain gives more control back to individuals:

- You own your digital identity and data.

- You can participate in financial systems without needing a bank account (especially useful in underbanked regions).

- You can verify ownership of assets (like art, music, or even real estate) through blockchain-based digital records.

6. A Foundation for Future Innovation

Just like the internet changed how we communicate and do business, blockchain is laying the groundwork for the next generation of digital services. From decentralized finance (DeFi) and non-fungible tokens (NFTs) to voting and transparent charities, the possibilities are endless.

Challenges of Blockchain

Whereas blockchain technology offers energizing benefits like security, straightforwardness, and decentralization, it’s not without its challenges. Like any developing technology, blockchain has a few obstacles to overcome some time recently it can reach its full potential. Let’s take a look at the key issues.

1. Scalability

One of the greatest challenges is adaptability — the capacity to handle a huge number of exchanges quickly.

- For example, Bitcoin can prepare around 7 exchanges per moment, while Visa can handle thousands.

- As more clients connect a blockchain arrange, it can gotten to be slower and more costly to use.

Solving this issue is basic if blockchain is to be received on a global scale.

2. Energy Consumption

Some blockchain networks, particularly those that utilize Proof of Work (PoW), require enormous sums of electricity.

- Bitcoin mining, for occurrence, employments more vitality than a few little countries.

- This raises concerns about environmental sustainability.

Newer models like Proof of Stake (PoS) are more energy-efficient, but the transition takes time.

3. Regulation and Legal Uncertainty

Since blockchain is still a generally new technology, laws and controls are not however clearly defined in many countries.

- This creates instability for businesses and developers.

- Governments are still figuring out how to control cryptocurrencies, smart contracts, and blockchain-based platforms.

Lack of clarity can moderate down adoption and innovation.

4. Complexity and Lack of Understanding

Blockchain is a complex concept, particularly for non-technical users.

- The learning curve can be steep.

- Many people still relate blockchain as it were with cryptocurrencies, not realizing its wider potential.

For blockchain to become standard, there needs to be better education and more user-friendly applications.

5. Security Risks (Not the Blockchain Itself)

While the blockchain itself is secure, the apps and systems built on best of it can be vulnerable to hacking.

- Poorly written smart contracts can be exploited.

- Cryptocurrency wallets and trades can be hacked if not properly protected.

Security in blockchain isn’t fair about the chain — it’s about the whole ecosystem.

6. Data Privacy

Blockchain is transparent by design, which is great for believe, but not perfect for sensitive data.

- Once information is included, it’s there forever.

- This makes a strife with protection laws like the “right to be forgotten” in controls such as GDPR.

Finding a adjust between transparency and privacy is a key challenge.

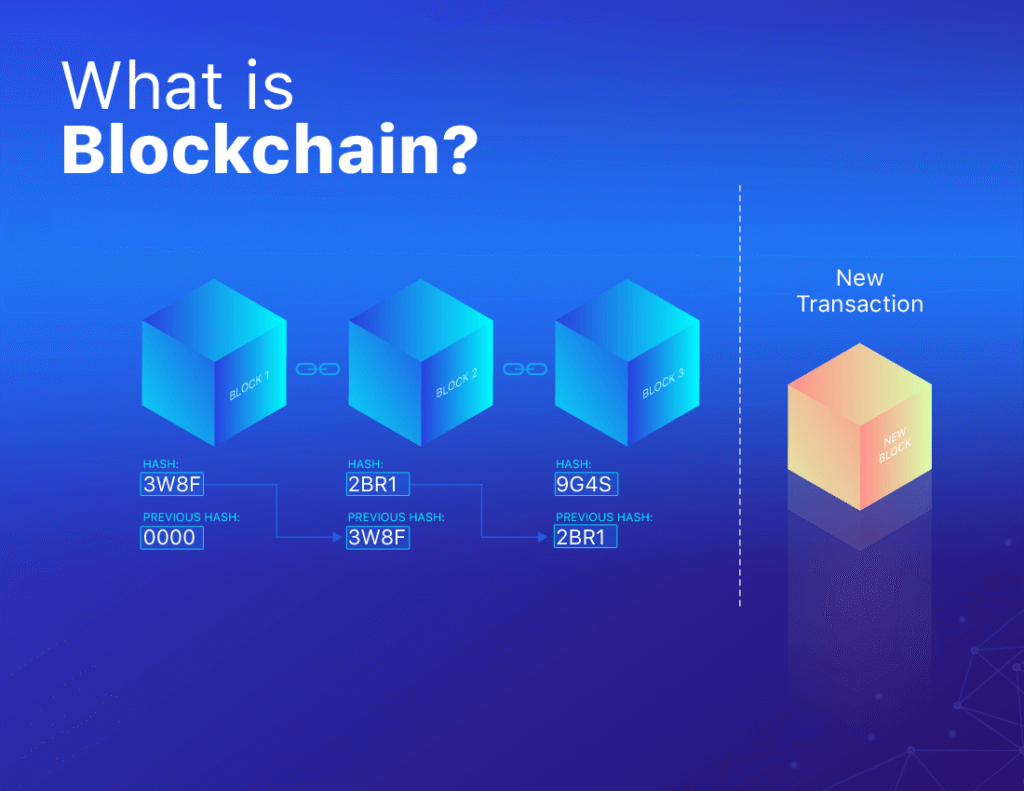

Future of Blockchain

Blockchain technology is still in its early stages, but its potential is massive. Just like the internet transformed how we communicate and do business, blockchain is set to redefine how we handle data, trust, and transactions. Let’s explore what the future might look like as this technology continues to evolve.

1. Mainstream Adoption

In the coming years, blockchain is expected to move from a niche innovation to a mainstream technology. As businesses, governments, and consumers begin to understand its value, we can expect:

- More blockchain-based apps and platforms

- Wider use in industries like healthcare, real estate, finance, and supply chain

- Seamless integration into daily life — often without users even knowing they’re using blockchain

2. Government and Public Sector Use

Governments around the world are exploring ways to use blockchain for secure digital identities, transparent voting systems, and even issuing digital currencies (CBDCs).

Example:

- Countries like China, Sweden, and India are actively testing or rolling out central bank digital currencies powered by blockchain-like technology.

3. Advancements in Scalability and Efficiency

Technology is advancing rapidly to address current limitations:

- Layer 2 solutions (like the Lightning Network for Bitcoin) help process transactions faster and cheaper.

- Next-generation blockchains (like Ethereum 2.0 and Polkadot) are being built to scale efficiently, use less energy, and support more complex applications.

These improvements will make blockchain systems more practical for everyday use.

4. Growth of Decentralized Finance (DeFi) and Web3

We’re entering the period of Web3 — a decentralized internet fueled by blockchain. This includes:

- DeFi (Decentralized Finance): Banking without banks — where users can lend, borrow, and trade assets on blockchain platforms.

- NFTs (Non-Fungible Tokens): Digital ownership of art, music, real estate, and more.

- DAOs (Decentralized Autonomous Organizations): Internet communities that run projects collectively, without traditional leadership structures.

These innovations are creating new business models and income opportunities around the world.

5. Improved Security and Privacy Features

Future blockchain platforms will likely include stronger privacy protections using advanced cryptography, allowing for secure transactions that protect personal data. This will be especially important in industries like healthcare, legal services, and personal finance.

6. Greater Collaboration Between Tech and Regulation

To thrive, blockchain must work alongside clear regulations that protect users without stifling innovation. Expect to see:

- New legal frameworks for cryptocurrencies and digital assets

- International cooperation on standards

- Better compliance tools built directly into blockchain systems

Conclusion

Blockchain technology is more than just a buzzword — it’s a powerful innovation that is transforming how we store, share, and secure information. What started with cryptocurrencies like Bitcoin has now evolved into a foundation for a wide range of applications across finance, healthcare, supply chain, voting systems, and beyond.

As we’ve explored in this guide, blockchain works by creating a secure, transparent, and decentralized record of transactions. Its key components — such as blocks, nodes, and consensus mechanisms — make it trustworthy and nearly impossible to tamper with. Despite current challenges like scalability, energy consumption, and legal uncertainty, the technology continues to improve and expand into new areas.

For beginners, understanding blockchain may seem overwhelming at first, but as with any technology, taking the time to learn the basics is the first step toward unlocking its potential. Whether you’re an person curious about how it works or a trade owner investigating new openings, blockchain is a drift worth paying attention to.

In the near future, blockchain could become as common and essential as the internet itself, changing the way we interact, do business, and build trust online.